Adobe PDF

Adobe PDF Microsoft Word

Microsoft Word OpenDocument

OpenDocument

Key Features

- Enhances Credibility. Reinforces seriousness and legitimacy, thereby increasing the likelihood of a debtor’s response and even cooperation.

- Improves Clarity. Reduces the chance for misunderstandings by explicitly detailing debts and options.

- Professional Formatting. Maintains Fair Debt Collection Practices Act (FDCPA) compliance while remaining customizable.

- Consistent Language and Tone. Maintains professionalism with a neutral tone and avoids non-compliant language.

- Good Recordkeeping. Utilizing a professional template helps keep track of collection efforts, especially when building a paper trail.

How to Remedy (7 steps)

1. Verify Compliance

2. Initial Contact

3. Required Validation Notice

4. Handle A Dispute

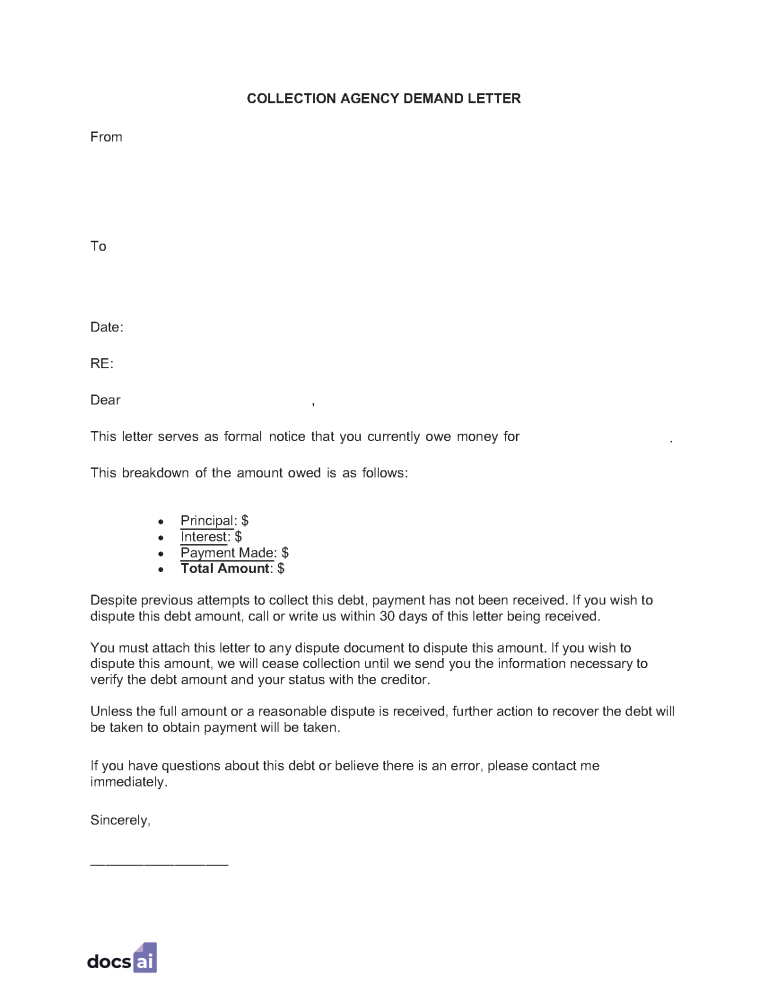

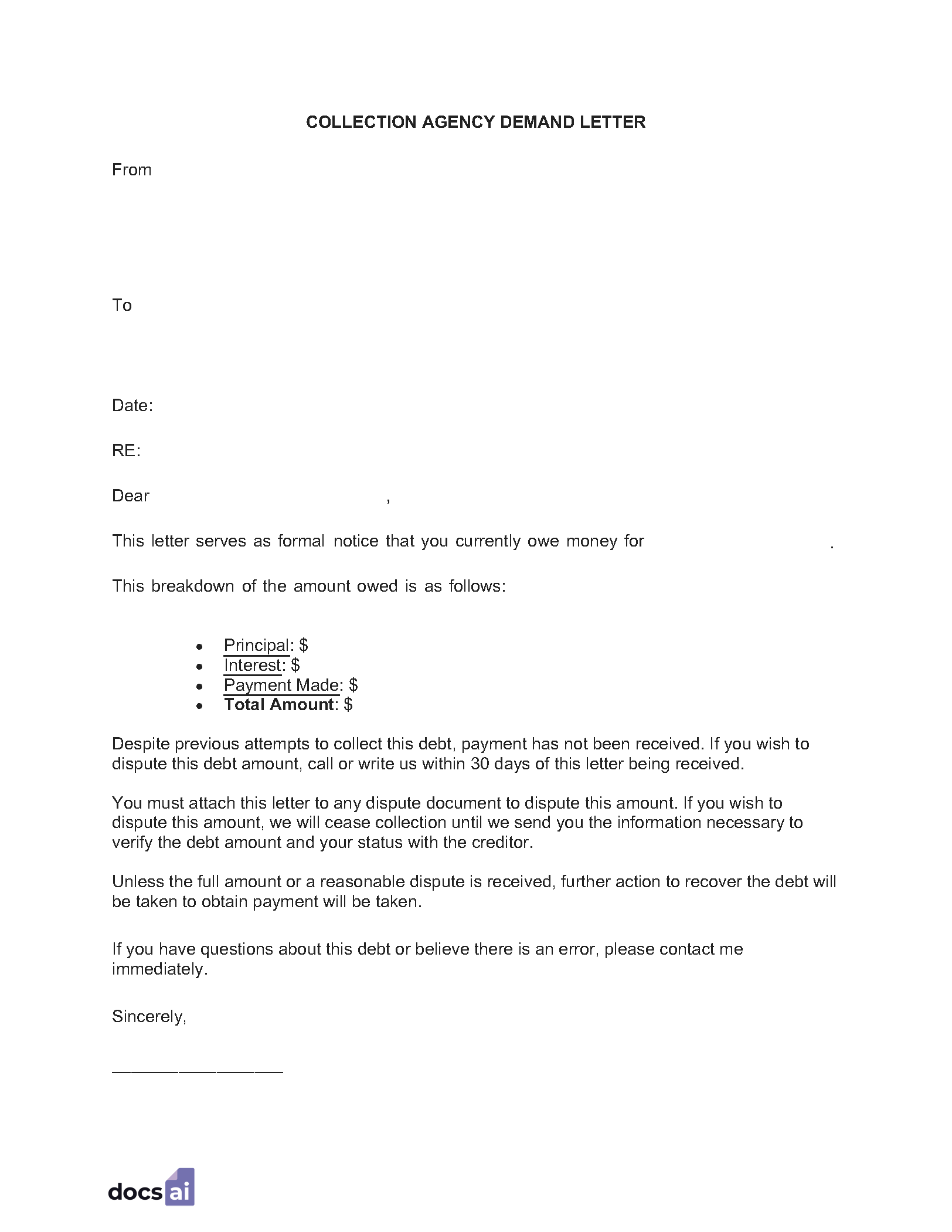

5. Send The Demand Letter

Once the thirty-day dispute period has passed, the agency sends a demand letter if the debt remains unresolved, especially if litigation is anticipated. This must include;

- Collection agency name, contact information, intent, and status

- Debtor’s identity and contact information

- Information identifying the original creditor(s)

- Source of the debt, total owed, an itemized explanation of the total, and a due date

- Instructions to respond with payment, negotiations, or dispute

- Disclosures that are required by federal and state laws.

6. Maintain Compliance If Escalation Is Needed

7. Updating Consumer Credit Report

Sample

-

Yes, but the debtor must consent to electronic communications (as per the E-Sign Act) and it complies with the Fair Debt Collection Practices Act (FDCPA).

-

Three years (minimum) as per the Fair Debt Collection Practices Act (FDCPA) and Consumer Financial Protection Bureau (CFPB) guidelines.

-

Yes, however, it must always comply with local, state, and federal laws while remaining appropriate to the circumstances, debt, and intent.

-

Yes, debtors must be given thirty days from receipt to dispute the debt. If disputed, all collection efforts must pause until verification is provided.

-

Yes, it can include a payment plan option or even a settlement, while remaining compliant with all applicable statutes (e.g., required legal disclosures).

-

Lawsuits can be pursued by the debtor, and the agency may be responsible for up to $1,000.00 in statutory damages per violation (FDCPA § 813).